NRIs can grab highest risk-free payouts before this exclusive RBI window closes

Updated: Jun 19th, 2026

Following a series of special capital-inflow measures announced by the Reserve Bank of India (RBI), prominent commercial and private lenders across India have aggressively hiked interest rates on Foreign Currency Non-Resident (Bank), or FCNR(B), deposits. Under this special policy window, the RBI temporarily lifted standard interest rate ceilings and agreed to absorb the currency hedging costs that Indian banks traditionally pay to secure foreign deposits.

By eliminating this hedging friction, the central bank has enabled domestic lenders to offer unprecedented, risk-free returns directly in foreign currencies. For Non-Resident Indians (NRIs) looking to grow their global savings with absolute capital safety, this targeted policy window represents a lucrative fixed-income opportunity.

High returns offered by various banks

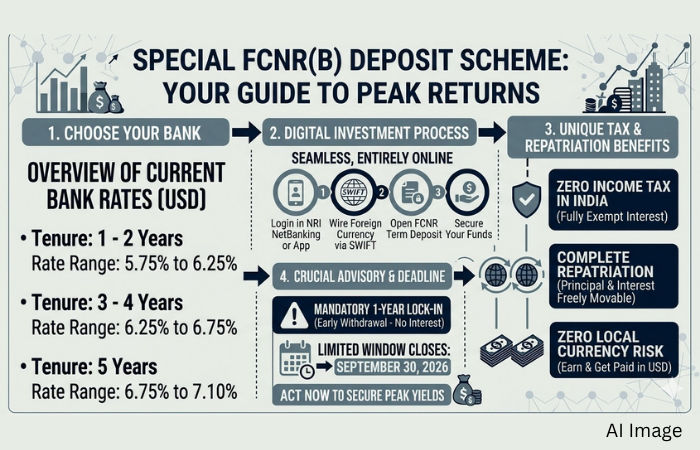

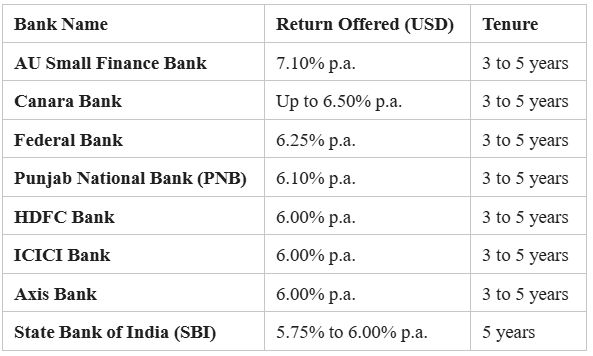

To take advantage of the RBI's specialized swap facility, multiple banks have rolled out distinct, limited-period FCNR schemes offering sharp rate jumps on US Dollar (USD) deposits, specifically for tenures spanning 3 to 5 years.

The limited-time window

The promotional interest rates are available for a strict, short-term window. The special regulatory relaxations became operational in June 2026, and the window is scheduled to close on September 30, 2026. Fresh deposits or renewals initiated after this deadline will revert to standard, lower interest rates (typically around 3% to 4%), as individual banks will have to bear their own hedging costs again. To lock in these peak yields, the deposit must be successfully processed before the deadline.

Step-by-step investment process

Investing in these high-yielding special deposit accounts is fully digitized and seamless for overseas citizens:

• Step 1: Choose Your Gateway: Log into your existing Indian bank's NRI internet banking portal or mobile application. If you do not have an active NRI account, you can apply digitally via the bank's overseas onboarding desk.

• Step 2: Transfer Funds: Wire your preferred foreign currency (such as USD) directly into India from your overseas bank account via SWIFT or an authorized digital exchange service.

• Step 3: Establish the Term Deposit: Select the dedicated "Open FCNR Term Deposit" tab, lock in a maturity period between 3 to 5 years to maximize yield, and specify your funding currency.

• Step 4: Note the Absolute Lock-In: All special FCNR accounts come with a mandatory one-year lock-in period. Withdrawing your capital prior to completing 12 full months clears out all accumulated interest earnings.

Tax and repatriation implications

The unique legal positioning of an FCNR account offers distinct tax shields, making it highly capital-efficient for global Indians:

• Zero Tax Liability in India: Interest income earned from an FCNR account is completely exempt from Indian Income Tax under current domestic regulations. Lenders will not execute any Tax Deducted at Source (TDS) on your accrued payouts.

• Free and Complete Repatriation: Both your original principal capital and the net compounded interest earned are 100% freely repatriable back to your home country. You do not require tax clearance certificates or central bank approvals to shift this money back overseas.

• Zero Local Currency Risk: Because you place funds in a foreign currency and receive payouts in that identical foreign currency upon maturity, you face no exchange rate depreciation risks. Any fluctuation in the value of the Indian Rupee (INR) during your tenure will not affect your ultimate return.

• Overseas Tax Clause: While India shields your earnings from tax, the interest you generate remains subject to the native tax rules of your country of residence (such as US Federal/State income taxes) and must be filed appropriately.